WTW | Charting a path forward in South-East Asia’s solar revolution

July 31 2023

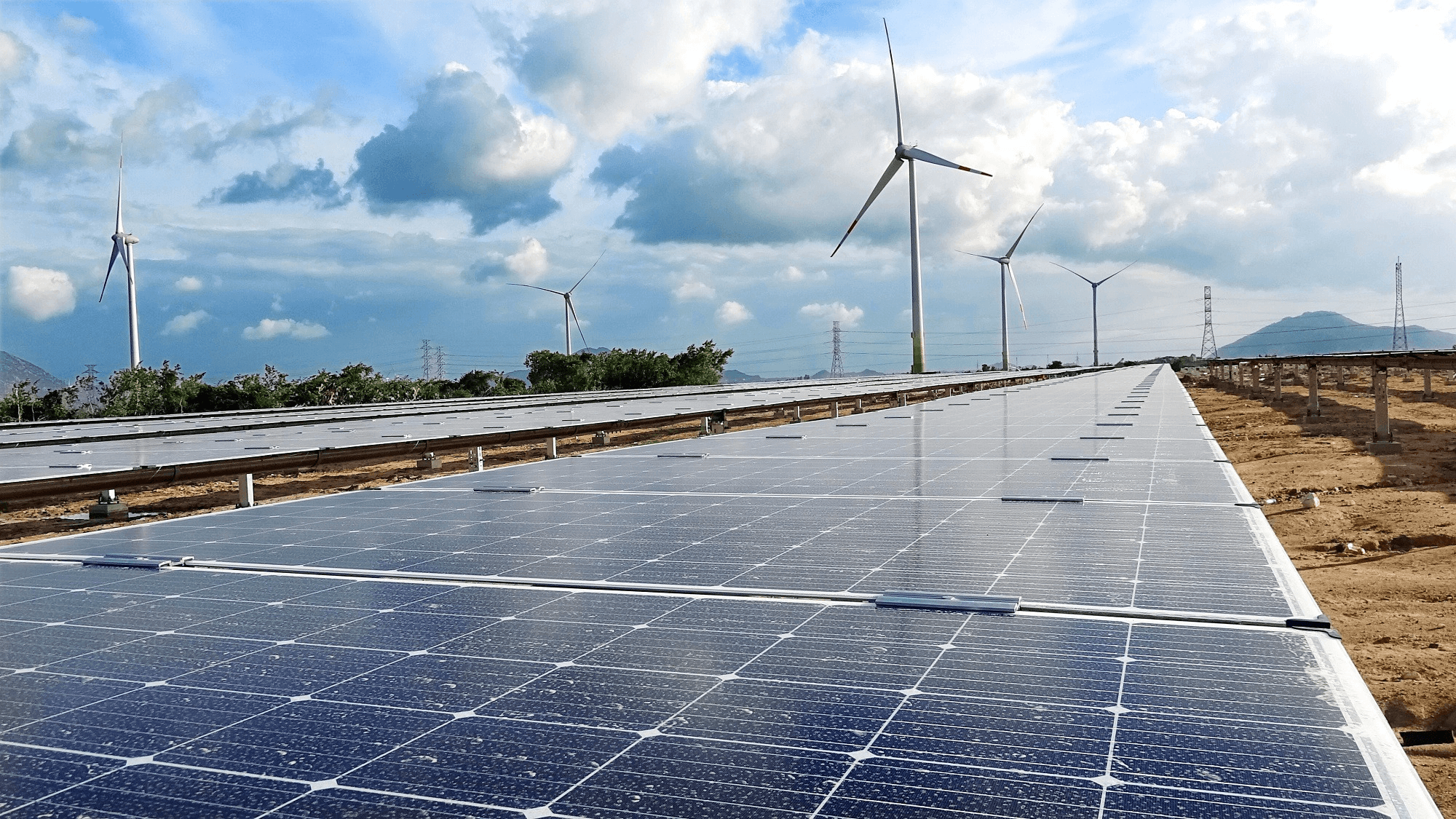

South-East Asia is now well on the way towards a greener future. Pioneering countries like Singapore, Vietnam and the Philippines have all taken proactive steps to accelerate the green transition, embracing cutting-edge technologies to deliver on ambitious net-zero targets.

Amongst which, the boom in solar technologies has been nothing short of remarkable. Installed solar power capacity in South-East Asia more than doubled from 10.4 GW to 22.9 GW between 2019 and 2020, according to the International Renewable Energy Agency (IRENA). Going forward, the Asean Centre for Energy forecasts, solar will see the highest generation capacity growth rate among renewable energy sources well into 2040.

While these figures point to a promising future for solar, the region’s renewable energy demand and transition ambitions are quickly outpacing its current development trajectory. Without policy interventions, the region’s renewable energy share is projected to reach just 14.4% of the total primary energy supply by 2025, missing the 23% target set in the Asean Plan of Action for Energy Cooperation 2016-2025 Phase II. This then begs the question, what steps need to be taken to turn hype into reality?

In my view, there are two lingering challenges that stand in the way of unlocking the full potential of South-East Asia’s solar market: the further facilitation of capital flows into regional solar infrastructure and rethinking supply chains in favour of resilience, as well as cost efficiency.

Making solar investable and insurable

The persistent funding gap facing South-East Asia’s green transition has been well-documented over the years. IRENA recently estimated that an average annual investment of US$210 billion to 2050 would be needed for Asean to align with pathway targets limiting global warming to 1.5 degrees Celsius – more than two and a half times the amount currently earmarked by regional governments. While more investors and insurers are entering this market to bridge the gap, tangible headwinds remain.

First, renewable energy regulations evolve quickly, often struggling to find the right balance between the short-term needs of stakeholders and long-term aspirations for sustainable growth in the process. Indonesia’s bumpy journey toward achieving a 23% share of renewables in its energy mix by 2025 highlights some of these challenges. Reluctance to wean the country off fossil fuels in favour of blended biomass co-firing in existing coal plants, widely held perceptions of higher costs for renewable energy infrastructure, and inflexible offtake contracts that often fall short of international standards, are all hindering Indonesia’s energy transition.

Investors and insurers need a clear view of the regulatory and policy landscape to make informed decisions. South-East Asia’s track record on this front has been mixed, but recent developments like the launch of the Just Energy Transition Partnership at the G20 Summit in November 2022 and the Asean Taxonomy for Sustainable Finance Version 2 in March 2023 could mean a coordinated long-term roadmap is on the horizon.

Second, renewable energy backers still lack access to adequate insurance coverage. South-East Asia’s susceptibility to natural catastrophes poses significant physical risks for renewable energy projects. As the number of new infrastructure developments and severe natural disasters increases concurrently, the strain on the insurance market will become more apparent. As a result, insurers are expected to tighten capacity for natural catastrophes and risk coverage in the coming years.

Beyond this, traditional insurance solutions often fail to cover financial losses resulting from unfavourable weather conditions affecting energy generation output. This is an important consideration when assessing a renewable energy asset’s potential revenue stream and resulting credit risk.

Indeed, the vulnerability of these cashflows to sub-optimal environmental inputs can ‘make or break’ a project’s long-term viability if improperly managed. Without proof of physical loss or damage, businesses have largely had to absorb this risk alone.

Weather parametric-based solutions could address both insurability challenges. Pay-outs for these insurance offerings are triggered by the value of an index, such as those modelling energy outputs or the probability of a certain pre-defined event happening. We are already seeing lenders add parametric insurance to loan terms in a few Asean markets; this will become an increasingly important lever in mitigating the risks and supporting the bankability of renewable projects.

Finally, the rising complexity of renewable energy technologies presents unique challenges to investors and insurers. The solar energy systems on the market today have moved far beyond the traditional ground-mounted installations to include advanced options such as floating solar farms installed in the open sea environment and hybrid solar-plus-storage solutions.

Additionally, the integration of solar energy into smart grids and the use of cutting-edge materials like perovskites have raised the bar for efficiency and performance.

As these advanced technologies continue to evolve, they demand more specialised knowledge and understanding of the associated risks. This will play a crucial role in shaping the future of renewable energy but may also lead to insurability concerns and thus creating new barriers to entry for capital.

Rethinking supply chains for resilience and cost efficiency

From WTW’s conversations with energy leaders worldwide, supply chain risks are a leading concern for their operating businesses and the continued viability of the green transition. Project times are lengthening, and costs are spiralling as companies compete to get raw materials and equipment, putting future transition plans at risk.

In a recent Energy Supply Chain Risk survey conducted by WTW, over two-thirds of executives echoed this sentiment, saying that supply chain-related losses were higher or much higher than expected in the past two years.

Likewise, Asean member states have also begun recognising that energy security and independence will depend on the resilience of renewable supply chains – both upstream and downstream.

However, current and future capacity for many critical inputs are geographically concentrated, with China dominating over 80% of all critical manufacturing stages for solar panels. South-East Asia, in contrast, holds only a modest share of the global solar supply chain.

As regional governments work towards greater energy security and corporates push to optimise their supply chains worldwide, the region can capitalise on its manufacturing capabilities and access to primary mineral resources to enhance its production foothold. The notion is not as farfetched as you might think. McKinsey estimated that South-East Asia has a 16-terawatt potential for manufacturing solar photovoltaic technologies. In fact, Thailand, Vietnam, and Malaysia already contribute around 10% of the world’s production of photovoltaic cells and modules.

To elevate the region’s status to a solar supply chain powerhouse, international and regional cooperation will be key. An important part of this process, where we see significant interest brewing, is getting a better understanding of the current state of supply chains. These can be through diagnostic mapping, data analytics, and monitoring tools to empower decision-making and communication between suppliers, manufacturers, and end users.

Realising solar’s full potential in South-East Asia

South-East Asia has the potential to become a global leader in solar energy. Realising this potential, however, requires a serious examination of lingering challenges. Governments and industry stakeholders must continue to work together to find a way forward in these areas. If done correctly, the long-term benefits to the region will be immense, offering new avenues for jobs, skill development, investment, and economic growth.

Get it wrong, we could miss a once-in-a-lifetime opportunity to secure its sustainable future.

|

Sam Liu

Director, Renewable Energy, Corporate Risk & Broking Asia, WTW

Email: [email protected] |

-

HSBC Asset Management | The hunt for diversification and performance revitalizes appetite for Asian currency bonds

With diversification and performance high on investors’ agendas, it seems a good time for global portfolios to revive allocations in Asian local currency bonds – including Hong Kong dollar (HKD) bonds.

-

PineBridge Investments | Why Asian insurers are exploring private credit and CLOs

The recent rollout of risk-based capital regimes across Asia calls for a closer alignment between insurers’ assets and liabilities. We explore potential ways to maintain a healthy investment yield and robust returns on regulatory capital.

-

Peak Re | Emerging Asia middle class: A catalyst for change

Rising demand for elderly care and women driving consumption growth mandate carriers to develop precise solutions to meet customer expectations.

-

Guy Carpenter | Private equity’s reshaping of the Asian life sector has further to run

PE-backed reinsurers provide access to asset classes and investment expertise that often don’t exist within the traditional carriers themselves.